Digital Marketing - Study Notes:

Payment providers

A really important part of this process is the payment providers. These are the people who provide the software that sits behind the website that takes the payment details from the customers, processes the transaction, and then passes the payment on to the retailer. And they do all this in a safe and secure way that are trusted by shoppers. Just imagine how difficult it would be if you were having to do all that coding of this new process, passing on that really sensitive data yourself in the coding of your website. And so, this is a really good example of where it’s best to outsource that bit of software engineering to these proven experts that know what they’re doing and that people trust.

Types

Now let’s take a look at the different payment types available. So, obviously, there’s things like credit cards, debit cards, and e-wallets, but within each of these is also different providers. So you’ve got the likes of American Express, MasterCard, and Visa. And you’ll sometimes see on different websites that some of these are available, and some of them aren’t, and why is that?

Settlement terms

Fees

Well, the key reason is that each of these providers apply different terms and conditions, and crucially, different fees, to the people using their product. So, American Express is often the one that you won’t be able to use, and the reason for that is that their fees are higher than some of the competition. So every time a retailer, or a customer, places a sale through an e-commerce site using an American Express card, the charge for that retailer will be higher than the charge if they were using a Visa card, and even higher than if they were using a debit card. So these are things that retailers will often consider about which types of card they want to accept based on the cost that they know they’ll be charged by the provider.

Fees to consumers

The other interesting thing is that there are sometimes different category norms between different categories. So, for example, you may well have booked a flight recently, and you’ve seen the standard price of your flight, and if you want to use a credit card, there’s an additional fee. This is because that airline is passing on the fee that the credit card charges them on to the consumer, in this case, you, whereas if you go to a clothing website, it’s very unlikely that you’d be asked to pay an additional fee to use a credit card. So again, it’s important to understand all these different nuances so that you can either decide to pass the cost on to your consumers, or make sure it’s built into your overall cost structure. And again, it’s about getting a balance right between providing the best possible and most convenient service to your customers, but also making sure you do it in a profitable way.

Terms for retailers

So, we’ve looked at how payments are taken from the consumers to the retailer, now let’s look at how payments are made between the retailer and the payment providers.

So there are typically some common terms and conditions associated with this, and they kind of fall into three categories:

- The length of time it takes to get a payment from the payment provider after the sale’s been made

- The percentage fee they’re going to take for each of those transactions

- In the event of a return or a complaint, how much of the fee that is clawed back to the end customer

These are all things that you’ll want to weigh up when you’re choosing which payment provider you want to use, and pick one that best aligns with your business objectives.

The other key consideration is how these different payment methods fit the markets you’re planning on operating in, and how they’ll also fit the markets you plan on growing into, because there are different consumer understandings and consumer expectations in different markets. For example, in some countries, the vast majority of customers pay with a Visa or a credit card, where in other developed markets, like Germany, there’s a much higher percentage of cash on delivery. There, people actually pay for the product when they receive it, rather than when they make the initial purchase. And again, these are things it’s important for you to understand so you can plan accordingly.

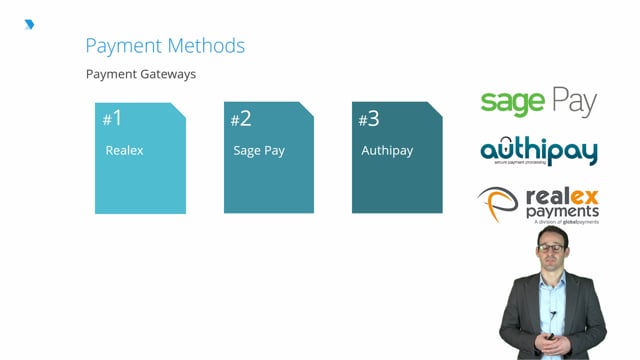

Payment gateways

So, we’ve already spoken a little bit about payment gateways.

The definition of a payment gateway is an e-commerce application service provider that authorizes credit card payments for e-businesses.

Common online payment gateways include:

- Realex

- Sage Pay

- Authipay

It’d be worth taking a little bit of time for you to go and have a look at each of these, and look at the different pros and cons of each of them, and deciding which is most relevant for you.

Back to TopGraeme Smeaton

Graeme Smeaton is the founder of Royal & Awesome. Along with a proven track record in defining and delivering marketing strategies that drive significant growth and create real shareholder value, Graeme is highly commercial. He has extensive experience managing PLs and other key financial statements, while being an operational board director of AFG Media Ltd, and has experience negotiating with suppliers, distributors and licensing partners.

By the end of this topic, you should be able to:

- Identify the impact of logistics, packaging, purchasing, distribution, and payment options for an e-commerce solution

- Evaluate e-commerce revenue models and the advantages associated with different e-commerce solutions

- Critically appraise the requirements for managing e-commerce customers in accordance with current laws and legal guidelines